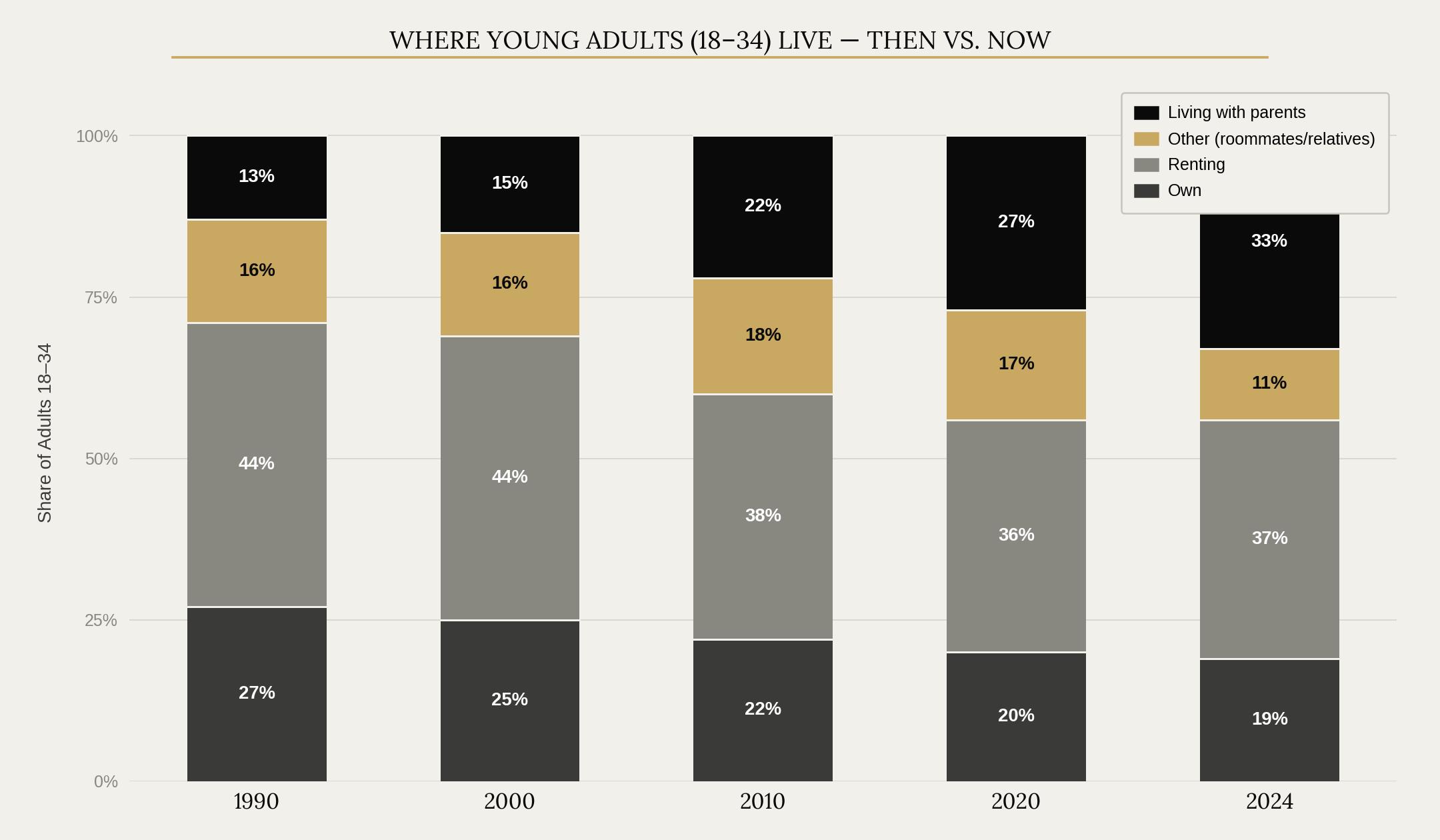

Here's a number that should make every NH landlord sit up: 1 in 3 adults under 35 in America is still living with their parents.

According to the most recent Census data, 32.5% of adults aged 18–34 lived with their parents in 2024 which is up from 31.8% the year before.

WHAT DOES THIS MEAN TO RENTERS

There's a massive cohort of would-be renters sitting on the sidelines — not by choice, but because the math doesn't work. To buy a home in New Hampshire without being cost-burdened, a household needs to earn around $158,000 a year. The median income is nowhere near that. Nationally, the monthly cost of owning has reached roughly double what comparable renters pay — a gap we haven't seen in modern history.

So people wait. They stay home. They rent with roommates. They delay the lease they actually want.

WHEN THEY MOVE OUT – THEY RENT

Here's the other half of the equation: new supply nationally is falling off a cliff. Multifamily construction starts fell to a seasonally adjusted annual rate of 284,000 units in May - a shadow of the 670,000 unit peak we saw in 2024. NH never had a meaningful supply wave to begin with. Vacancy rates here remain well below the 5% level considered a balanced market.

But here's something the supply charts don't show: rents in NH aren't rising the way the fundamentals would suggest they should. Rents are essentially flat year-over-year despite vacancy staying extremely tight. The reason isn't lack of demand, it's that inflation has already stretched tenants close to their ceiling. When people are spending 30–35% of take-home pay on rent, there's only so much more you can ask for before they move in with family instead. In a market this constrained, that's the pressure valve.

What that means for landlords: the rent growth that supply and demand alone would justify isn't gone, it's deferred. As wage growth catches up to where costs have been sitting, that headroom opens back up. The supply setup is already in place. The demand is already there. It's just waiting on affordability to give it room to move.

Less supply coming. More renters in the pipeline. And a rent level that has more upside than the flat year-over-year numbers suggest.

WHAT I’M DOING WITH THIS

I'm not chasing rent growth right now. With tenants already stretched thin, the math on pushing rents is simple: you win a few extra dollars a month and you risk losing someone who's been paying on time for two years. Finding and qualifying a replacement costs more than the increase was worth - and that's before the turnover costs.

The focus right now is retention. Keep good tenants in place, keep units full, and don't give anyone a reason to move back in with their parents. In a market where the demand is real but the affordability ceiling is real too, vacancy is the enemy — not below-market rent.

The other thing I'm doing is locking in long-term debt wherever I can. If the thesis is right that rent growth is deferred, not gone then the operators who will capture it are the ones still standing when affordability finally opens back up. That means fixed rates, conservative underwriting, and not over-leveraging into a market that's still finding its footing. Patience is the position.

The supply setup is already in place. The demand is already there. This is a market you want to be in when conditions shift not one you want to be scrambling to enter.