Two things are true right now that most people treat as separate stories but are actually deeply connected: Americans are voting with their feet and leaving expensive states in record numbers, and mortgage rates are not coming down anytime soon.

THE NATIONAL AFFORDABILITY CRISIS IS REAL AND GETTING WORSE

The numbers are hard to argue with. Realtor.com's 2026 Housing Supply Gap report puts the national deficit at 4.03 million homes — up from 3.8 million in 2024, and the third-largest supply gap of the past 14 years. We've been underbuilding for over a decade, and even if construction jumped 50% from today's pace, economists estimate it would take seven years to close the gap.

The income picture is just as bleak. A household earning $75,000 a year — teachers, nurses, tradespeople, the people who actually make a community run — can only afford 21% of the homes currently listed for sale. Before the pandemic, that same household could afford nearly half. That's a fundamental change in who can participate in the housing market.

What's happening in the South and West makes this even clearer. Price cuts on new construction are spreading across Texas, Florida, Nevada, and the Carolinas — markets that overbuilt during the rate boom and are now working through a glut. But in the Northeast, new builds are a different story. They're scarce, they're not being discounted, and they're not going to be. Zoning, land costs, and labor constraints mean you simply can't build your way out of the problem here the way you might try to in Phoenix or Atlanta.

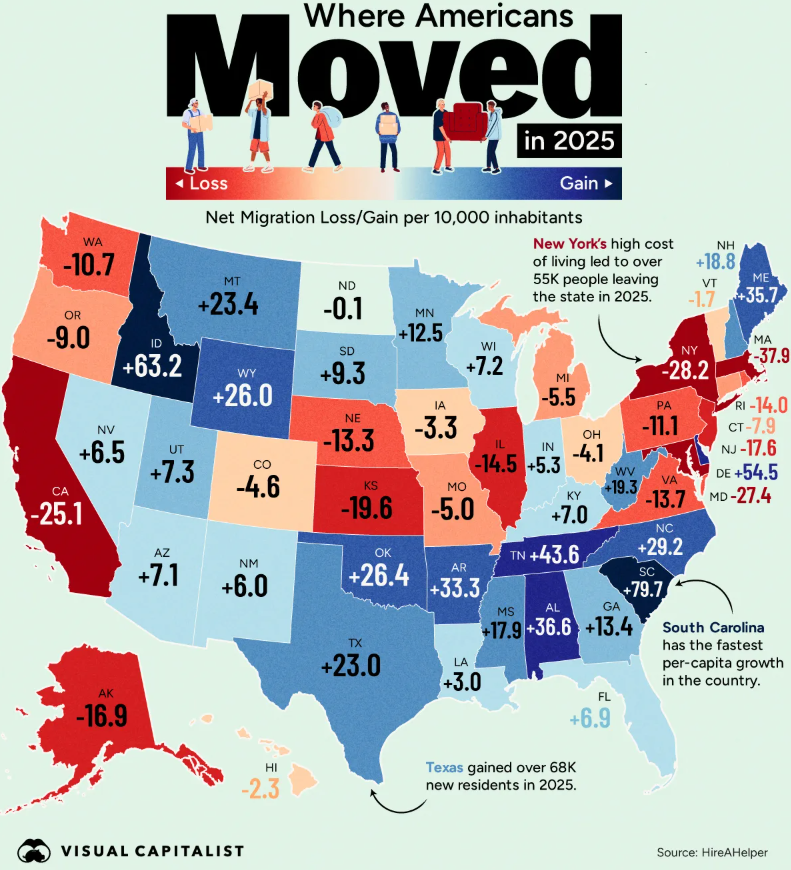

PEOPLE ARE RESPONDING BY MOVING — AND NH IS WINNING

When housing costs become prohibitive, people move. We're seeing this play out nationally, with smaller metro areas in New England, the Midwest, and other affordable corridors absorbing demand that used to flow into major cities. The rise of remote work unlocked this for a lot of people, and while some of the pandemic-era surge has normalized, the underlying trend has not reversed.

Nowhere is this clearer than the Massachusetts-to-New Hampshire pipeline. From 2010 to 2023, New Hampshire gained a net total of nearly 99,000 residents from Massachusetts — roughly enough to build another city the size of Manchester. Today, 25% of New Hampshire residents were born in Massachusetts. Massachusetts lost $10.6 billion in adjusted gross income to net out-migration between 2020 and 2022 alone. That capital is going somewhere — a meaningful chunk of it is going north on Route 93.

New Hampshire's population grew by an estimated 6,800 people between July 2024 and July 2025, and the state's entire net population gain now comes from in-migration. Deaths have outpaced births every year since 2017. What's sustaining the state's growth is people choosing to relocate here — primarily from Massachusetts — for lower taxes, more affordable housing, and access to the same Boston-area job market.

This is not a one-time COVID anomaly. The data from the NH Fiscal Policy Institute confirms that by 2024, net in-migration from Massachusetts had rebounded back to roughly pre-pandemic levels after a dip in 2023. The flow is durable and structural, driven by cost of living, not just by remote work flexibility.

WHAT THIS MEANS FOR SOUTHERN NH MULTIFAMILY

For those of us investing in the Nashua-to-Portsmouth corridor, this migration pattern is the thesis. We are sitting directly in the path of the most predictable, well-documented, sustained population flow in New England. These are not transient renters. These are people leaving Boston-area apartments, or selling smaller Massachusetts homes, who are coming to Southern NH to rent while they get their footing — or because they can't afford to buy here either, at least not yet.

The supply constraint in New Hampshire is real. We have strict zoning, limited developable land, a construction labor market that's as tight as anywhere in the country, and no meaningful pipeline of new rental supply in the 3–50 unit segment. Demand keeps coming. Supply isn't following. That's the most durable setup you can find in real estate.

RATES: STOP WAITING FOR THEM TO FALL

My second story is a bummer. It's mortgage rates, and specifically the growing number of people who keep telling themselves rates are coming down soon. They're not — at least not meaningfully, and not in 2026.

Inflation is the root cause, and it's not going away. The Consumer Price Index rose close to 1% in a single month. Oil prices, driven in part by everything happening in Iran, are spiking — and energy costs feed into almost every other inflation category. The Fed has already made the bulk of its cuts, and with a potential leadership transition at the central bank creating uncertainty, there's very little political or monetary cover for further easing.

Consumer sentiment just hit a 70-year low, which historically signals a slowdown in transactions but not necessarily in prices, because the same conditions that depress sentiment also depress new supply. For rates to come down materially, you'd need either a significant drop in inflation or the Federal Reserve to restart quantitative easing — buying mortgage-backed securities at scale. There's no evidence that's coming this year.

If you want to track this data in real time, Pensford publishes a SOFR forward curve (pensford.com/forward-curve) that shows you what the market is actually pricing in for rate movement — not what a pundit is hoping for. Right now, the curve is not projecting anything that should give a rate-watchers much optimism.

What does this mean practically? It means the investors who wait for a better rate environment to enter the market will likely still be waiting at year's end. It also means that the sellers on the sidelines who can't reconcile today's pricing with what their property was worth in 2022 are slowly running out of runway. In Southern NH, that's creating off-market opportunities worth paying attention to.

THE VIEW FROM HERE

I know, I know, none of this is very optimistic. Deals have to pencil at today's rates. Rent growth is real but modest. And the buyers in our market are working harder than ever just to break even on acquisitions. I get it.

But the structural case for Southern NH multifamily remains about as solid as I've seen it. Population growth is migration-driven and durable. Supply is constrained by geography and regulation. Affordability pressure is pushing renters into our market from both above (priced out of homeownership) and below (unable to afford Boston rents). And the institutional capital that has been waiting on the sidelines is starting to redeploy into the Northeast, which eventually puts a floor under valuations even if it doesn't directly move our sub-100 unit market.

The people waiting for perfect conditions before they invest are going to be waiting a long time.